The question of who owns 5G standard-essential patents is an issue that many institutions and companies are grappling with as this important technology gets deployed. Many have claimed through declarations that they own 5G essential patents, but there is currently no economically sensible way to evaluate these claims. At least when companies self-declare their 5G patents, they generally agree to license them on a fair, reasonable, and non-discriminatory (FRAND) basis, ostensibly limiting their use for securing injunctions and disproportionately high royalties. Unfortunately, experience with other standards teaches us that many potentially essential patents are never declared and are thus unencumbered by any FRAND obligations. This article identifies self-declared 5G patents and, more importantly, undeclared and FRAND-unencumbered patents, or 5G “submarine" patents.

3GPP Patent Declarations - Standards Participation vs. Declarations

According to OPEN, Unified Patents’ 3GPP standards submissions database, over 100,000 5G technical contributions have been submitted to ETSI as of March 2020. Of those, only 812 technical specifications were agreed upon, approved, or endorsed for the 5G standard, with roughly half of them submitted by just three companies: Ericsson, Huawei, and Nokia.

As of March 2020, these technical contributions have led to over 25,000 patent families (over 96,000 patents and applications) being self-declared as essential, as shown in Unified Patents’ AI-based landscaping tool OPAL. As a rule, participants in ETSI 5G standardization work are required to declare in a timely fashion any patents essential to a 5G technical specification, particularly any standard or specification where they participate. In their declarations, ETSI expects participants to specify the technical specifications to which the declaration is made. While this provides a wealth of data for evaluating potential essential patent ownership, the data is lacking on a number of fronts:

There is no independent review that declared patents and applications are essential or reference the correct technical specifications.

Participants are not required to conduct an exhaustive search for potentially essential patents.

The data can lag behind the official release of the referenced standard specification.

As discussed later, the data does not capture any potentially essential patents that were not declared by 3GPP standardization participants or which belong to entities that do not participate in 3GPP standardization work.

Existing tools should not be considered a landscape

A landscape inherently should include or model for all patents related to a technology area to accurately demonstrate each company’s market share. Many have released 5G tools; unfortunately, none of these tools do so, as their data is incomplete. Most—such as IPLytics—provide a database that only includes self-declared patents, with no assessment of essentiality or invalidity. Others, such as CPA and twoBirds Pattern, do attempt to filter for essentiality based on organic or court-adopted essentiality reviews but again, these only take into account the self-declared patents and applications. And the essentiality filters used by some of these tools are usually based on a potentially biased sampling of SEPs declared to 3GPP standards other than 5G. The percentage results of these reviews are also sometimes applied indiscriminately across all 3GPP participants’ portfolios, without regard to each participant’s declaration and patent prosecution processes.

The percentage of self-declared patents estimated by courts and experts to be truly essential ranges from 50% to lower than 20%. In 2005, Goodman and Myers found 21% of self-declared patents in 3G were essential. In 2010, Fairfield Resources estimated 50% of self-declared patents in LTE were essential. In the remanded US TCL vs Ericsson case, the court’s calculation resulted in about 40% of all 2G, 3G, and LTE self-declared patents being essential. Finally, in the UK Unwired Planet vs Huawei case, the court used 16.6% to calculate the number of essential LTE patents among all self-declared ones. If we are to believe that 5G will mimic previous 3GPP standards, the true landscape of essential patents will be much smaller than the number declared; the share of each company could change accordingly.

As noted, a landscape should not just take into account patents owned by 5G contributors under an obligation to self-declare, but also account for those potential patents owned by non-contributors to 5G (who have no obligation to self-declare). This would likely result in a demonstrably larger 5G landscape than the current studies, which only include self-declared patents. Until now, however, no 5G tool has addressed these undeclared patents. We seek to remedy that defect.

Counting Grants versus Applications

As of March 2020, about ⅔ of all self-declared 5G patent applications have not issued. It is misleading to count pending applications as being essential, as they may not be granted at all, or their claims may be amended so much during prosecution that they are not essential. At a minimum, any such studies should have discounted the overall applications by a prevailing grant rate, and controlled for essentiality. There is no evidence they did so.

Declaration Leapfrog

Who leads in 5G declarations also changes dramatically over time, given new declarations, grants, and other activity. The chart below shows how the various putative leaders in 5G declarations have leapfrogged each other roughly every six months. This leapfrogging will only continue as the number of declarations grows, and as the standard evolves. If the development of LTE and LTE-essential declarations is any measure, the number of patents and applications declared essential to 5G may ultimately increase manifold.

This can be shown historically through the submissions in OPEN and the correspondingly timed LTE declarations in OPAL. For example, from the end date for LTE Release 8 in March 2009 until March 2020, over 64,500 new draft technical specifications and reports and change requests and pseudo-change requests were submitted for consideration to the LTE standard. As shown in the OPEN submissions status graph below, over 8,000 of these submissions were either agreed to or approved after March 2009, and they, directly or indirectly, triggered the declaration of another 19,000+ potential LTE essential families with active patents and applications in major jurisdictions (i.e., US, CN, EP, JP, KR, WO) in addition to the 2,559 active major-jurisdiction families already declared in connection with LTE Release 8.

Using AI to Objectively Assess Essentiality

OPAL, on the other hand, can be considered a true 5G landscaping tool, as it measures 5G essentiality for all patents, rather than just those self-declared to 5G. OPAL uses AI to objectively evaluate any patent or application’s semantic similarity to all those that were self-declared. This allows users to identify potentially essential patents they would never otherwise find.

OPAL scores semantic similarity on a scale of 0 to 100. The higher the score, the closer a patent’s correlation to the semantics of self-declared 5G patents. OPAL was trained using a positive training set comprising all declared 5G patents and a negative training set comprising all declared patents in previous 3GPP standards not declared for 5G. For the purpose of this article, the similarity score was set at 75, as 50% of self-declared 5G patents are below that threshold, similar to what some studies have found when evaluating such patents for essentiality. OPAL then evaluated nearly 3 million patents with one or more CPC classes in common with any 5G self-declared patents.

OPAL found Huawei leads in total number of self-declared (2,100 families) and undeclared 5G patents at a score of 75 or higher. 70% of Huawei’s self-declared patents—3,005 5G families—achieved a score of 75 or higher, vs. only 50%, for example, for Blackberry.

Chinese Entities hold a Large Number of Submarine Patents

OPAL identified more than 21,000 families (76,050 patents and applications) as scoring above 75. Almost 95% belong to existing 5G declarants such as Samsung, Huawei, Ericsson, and Nokia. Of those, almost one-third have not been specifically declared, and thus may not be subject to FRAND unless an applicable general declaration has been made. As mentioned above, ETSI IPR rules require that participating members in 5G standards work use reasonable efforts to timely notify ETSI of any patents or patent applications that may be essential to the standard and in particular inform ETSI of any of their patents and applications that may be essential to a technical proposal that they have submitted should such proposal be adopted. Failure to notify ETSI of a potentially essential patent in a timely manner may signal that the patent holder has impliedly waived its rights to enforce the patent against 5G implementations. Conversant Wireless Licensing discovered this in its 2019 case against Apple on remand from the Federal Circuit. Not everyone agrees, however, that such a harsh consequence is warranted for a failure to notify a standards body of a potential standard essential patent or application as Asustek Computers discovered in 2019 in an adverse decision in the Court of Appeal of The Hague involving Philips.

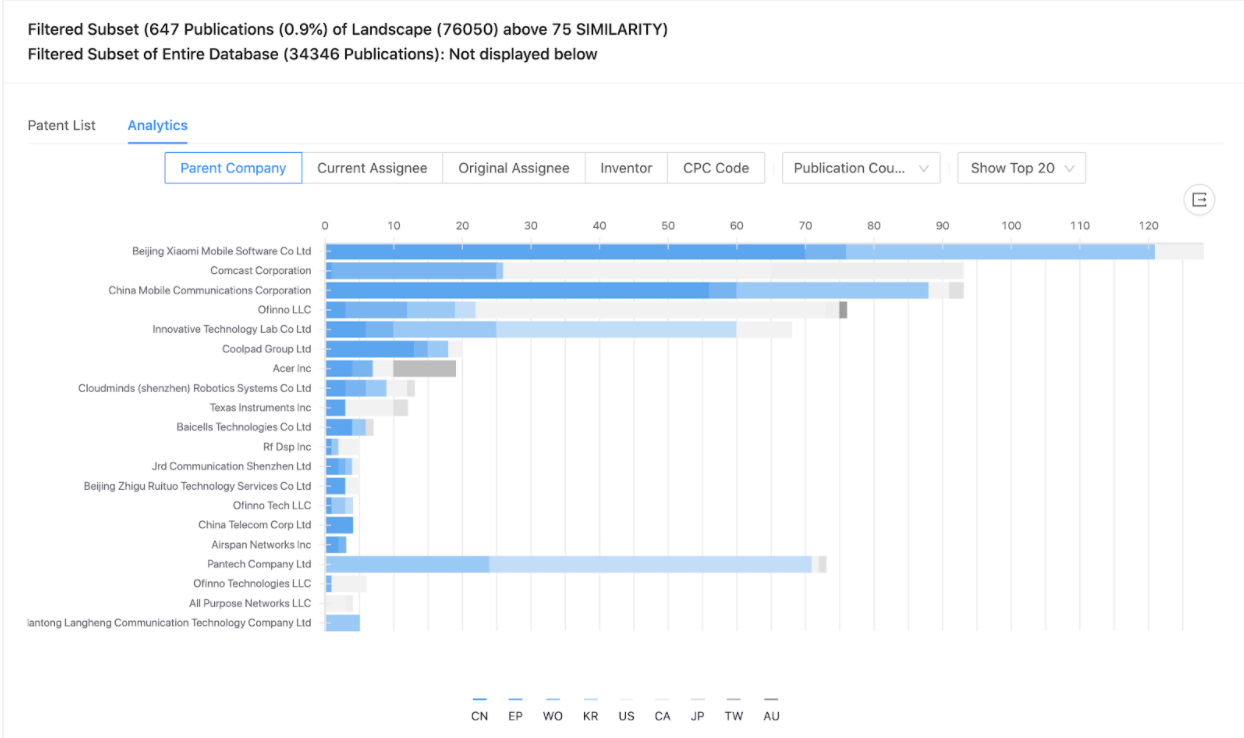

OPAL further found 1,000 patent families (5%) held by entities such as Xiaomi, Comcast, China Mobile, Acer, and Texas Instruments that self-declared few (if any) patents apparently essential to 5G or which did not participate in 5G standardization. These submarine patents have lurked unseen and, if they are truly unencumbered by any FRAND obligations, could significantly increase the cost of deploying 5G.

The first chart above lists the top 18 entities identified by OPAL as holding 5G submarine families and the jurisdictions in which they filed their applications. Altogether, these entities hold 362 families (647 grants and applications). The eight Chinese entities own 28%, while the six US entities own 21%. These submarine patents could be valuable targets for acquisition, licensing, or assertion, and could be useful in establishing reasonable royalty rates. Some of the holders of these submarine patents could be open to sales or licensing. For example, as shown in the second chart above, R&D entities such as Shanghai Langbo, Ofinno, and Innovative Technology Lab hold about half of these submarine patents, and they may need financing for their R&D activities. For example, Langbo recently transferred to Sisvel an LTE portfolio for monetization.

Conclusion

A complete IP landscape is needed to understand the licensing cost of 5G. Such a landscape like Unified’s OPAL should include an evaluation for essentiality and should not be restricted to just self-declared patents. Without such a landscape, it is difficult for implementers of 5G to understand the total licensing cost and whether offers made in licensing discussions are actually FRAND.